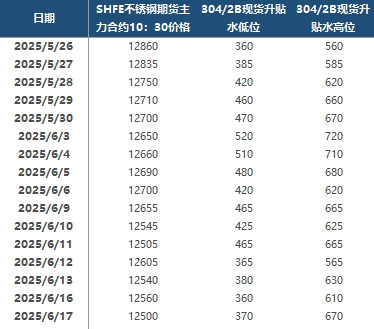

SMM News on June 16: Today, influenced by the decline in SHFE nickel, the SS futures market was weak, falling below the 12,500 yuan/mt threshold. Against the backdrop of continuously declining stainless steel prices, market confidence was shaken, with downstream players generally adopting a cautious wait-and-see attitude, focusing mainly on just-in-time procurement in small quantities. Spot market transactions remained sluggish. Recently, prices of both high-grade NPI and high-carbon ferrochrome have shown a downward trend, resulting in weak cost support for stainless steel. Currently, in the traditional consumption off-season, there is a general lack of confidence in the market regarding a consumption recovery. Despite stainless steel prices having fallen to low levels, the price reductions have not effectively stimulated transactions. Traders expect stainless steel mills to cut production to gradually restore the current supply-demand imbalance in the market.

In the futures market, the most-traded 2508 contract weakened and declined. At 10:30 a.m., SS2508 was reported at 12,500 yuan/mt, down 60 yuan/mt from the previous trading day. Spot premiums/discounts for 304/2B in the Wuxi region were in the range of 370-670 yuan/mt. In the spot market, cold-rolled 201/2B coils in both Wuxi and Foshan were reported at 7,750 yuan/mt; cold-rolled trimmed 304/2B coils had an average price of 12,850 yuan/mt in Wuxi and the same in Foshan; cold-rolled 316L/2B coils were priced at 24,000 yuan/mt in Wuxi and the same in Foshan; hot-rolled 316L/NO.1 coils were reported at 23,350 yuan/mt in both regions; cold-rolled 430/2B coils were priced at 7,500 yuan/mt in both Wuxi and Foshan.

Currently, the stainless steel market is deeply mired in the traditional consumption off-season, with continuously sluggish downstream demand. Despite enterprises generally facing losses, some steel mills have already implemented production cuts. However, due to the large production base in the early stage, current supply remains at a historically high level for the same period, with a prominent contradiction of oversupply in the market. Stainless steel mills and agents are facing increasing pressure to sell, with market pessimism spreading. Traders are competing to sell, pushing stainless steel quotes continuously lower. The raw material side is also under pressure. Influenced by expectations for production cuts at steel mills, the price increase of high-grade NPI has been hindered; the price of high-carbon ferrochrome continues to decline, further weakening cost support for stainless steel. If the subsequent production cut efforts fall short of expectations, against the backdrop of weak demand in the off-season, the pattern of stainless steel prices being in the doldrums in the short term is unlikely to change.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)